Mastering Volatility: Why ATR Position Sizing Outperforms Fixed Strategies in Dynamic Markets

Published on 3/22/2026While the allure of finding the perfect entry or exit point dominates much of trading discourse, a deeper dive into professional practices reveals a surprising truth: consistent profitability often hinges less on predictive accuracy and more on meticulous risk management. Indeed, industry estimates suggest that up to 90% of retail traders fail, with poor risk management — particularly inconsistent position sizing — frequently cited as a primary culprit. The stark contrast between amateur and professional lies in the approach to capital preservation, where the latter prioritizes controlling losses over chasing immediate gains. For this reason, understanding and implementing dynamic position sizing, such as that based on the Average True Range (ATR), is not merely an optimization; it's a fundamental shift towards sustainable trading.

Key Takeaways

- Position sizing, often neglected by retail traders, is a cornerstone of professional risk management, distinguishing consistent performance from speculative gambling.

- ATR-based position sizing dynamically adjusts trade size inversely to market volatility, ensuring a consistent dollar risk per trade regardless of market conditions.

- By scaling positions, traders can avoid the common mistake of overexposure during high volatility (where losses magnify) and underexposure during low volatility (where opportunities are missed).

- A common approach involves using a 14-period ATR, multiplied by a factor (e.g., 1.5 to 2x), to define stop-loss distance, then calculating position size based on a predefined percentage of account risk.

- ATR is versatile, working across all markets (stocks, forex, crypto) and timeframes, providing a volatility buffer that adapts to the trade's intended holding period.

The Neglected Cornerstone of Consistent Trading: Position Sizing

In the high-stakes world of trading, countless hours are spent perfecting entry signals, optimizing indicator parameters, and forecasting market direction. Yet, a critical component, position sizing, often remains an afterthought. This oversight can be detrimental, as holaprime.com notes, "Position sizing is one of the most neglected aspects of trading, but it is what distinguishes the professional from the hobbyist." While market analysis focuses on 'where' to trade, position sizing dictates 'how much' to trade, directly impacting capital preservation and long-term viability.

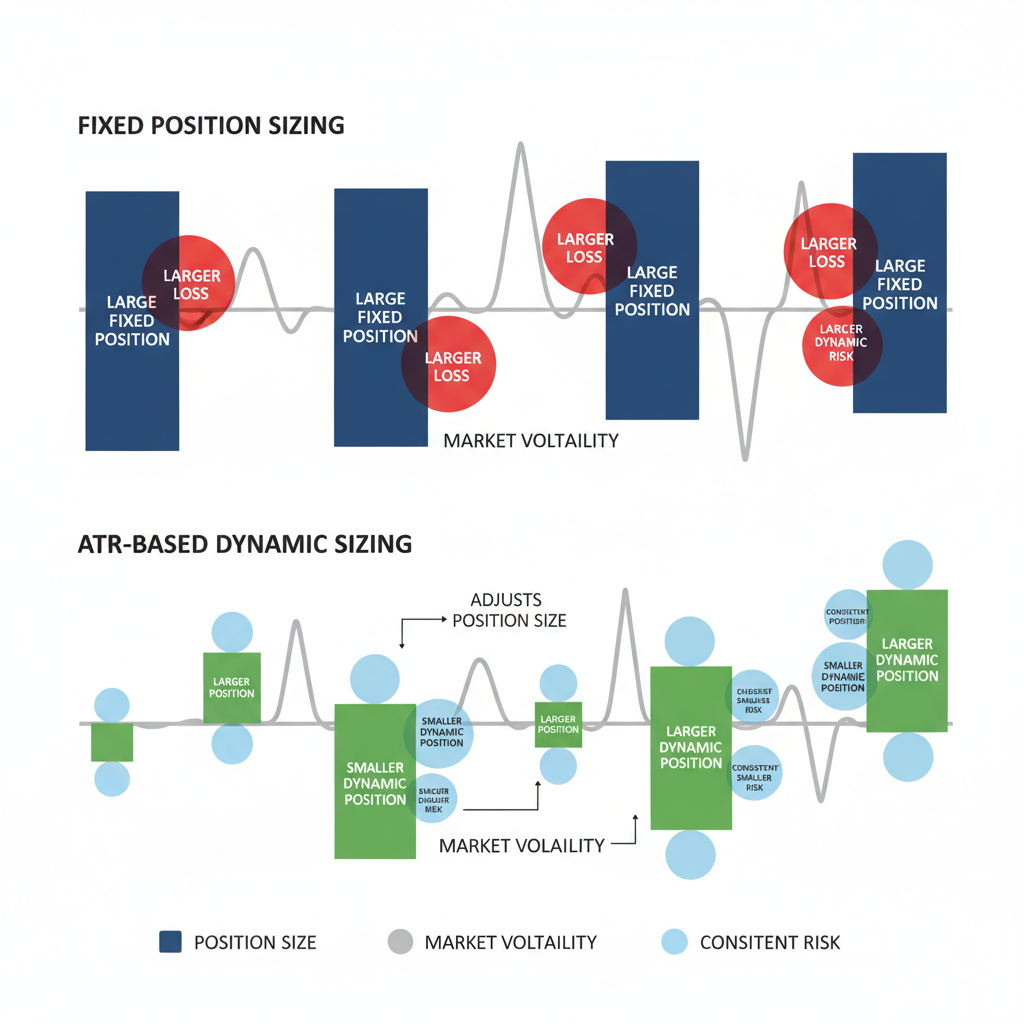

Many traders default to fixed position sizes, risking a set dollar amount or a fixed percentage of their capital per trade without accounting for varying market dynamics. This static approach can lead to wildly inconsistent risk exposure. For instance, risking a fixed $500 per trade might be appropriate in calm markets, but during periods of heightened volatility, such a position could represent a far greater percentage risk if stop-loss distances need to widen significantly to avoid being stopped out by normal market "noise." Conversely, in exceptionally quiet markets, the same $500 risk might be too small, limiting potential gains from a clear, low-volatility move.

Professional traders recognize that market volatility is not static. A fixed position size is akin to driving at a constant speed regardless of road conditions, an approach that is both inefficient and dangerous in dynamic environments. Therefore, a more adaptive strategy is essential for sustainable trading.

The goal is not to eliminate losing trades—which are an inevitable part of trading—but to ensure that these losses are manageable and survivable. As Holaprime highlights, "Your goal is to ensure those losses are managed and survivable, so you can trade again for the next opportunity." This necessitates a risk management framework that adjusts to prevailing market conditions, allowing traders to stay consistent across trades and avoid the extremes of overexposure or undertrading.

ATR: Volatility's Unbiased Compass

To dynamically adjust position sizes, traders need an objective measure of market volatility. This is where the Average True Range (ATR) indicator becomes invaluable. Developed by J. Welles Wilder Jr., ATR provides a smoothed measure of price volatility over a specified period, typically 14 periods (e.g., 14 days, 14 hours, 14 minutes), as commonly cited by sources like FXNX and Charles Schwab. Unlike price-based indicators, ATR focuses purely on the magnitude of price movement, including gaps, making it a robust measure of a market's "true" volatility.

The ATR calculates the largest of three values for each period:

- Current high minus current low.

- Absolute value of the current high minus the previous close.

- Absolute value of the current low minus the previous close.

These values are then averaged over the chosen period, resulting in a single number that represents the average price movement. For example, an ATR of 80 pips on a daily chart for EUR/USD signifies that, on average, the pair has moved 80 pips per day over the last 14 days. This is crucial because it offers a realistic gauge of how much a market typically moves, which directly informs stop-loss placement and, by extension, position sizing.

The versatility of ATR is a key advantage. Holaprime confirms, "Yes, ATR works across all markets since it only measures price movement. Whether it’s currency pairs, futures contracts, or stocks, ATR adjusts to volatility naturally." This makes it a universal tool for risk management, capable of adapting to the unique characteristics of different asset classes and timeframes.

Moreover, ATR offers a distinct advantage over other volatility indicators like Bollinger Bands. While Bollinger Bands measure standard deviation around a moving average, ATR measures average movement in points or pips, making it "easier to use for stops and position sizing" due to its direct translation into price units.

Dynamic Risk Adjustment: The Power of ATR Position Sizing

The core philosophy behind ATR-based position sizing is simple yet profound: maintain a consistent dollar risk per trade by inversely scaling position size to current market volatility. This means that when volatility is high, you take a smaller position, and when volatility is low, you can take a larger position, all while risking the same predefined dollar amount or percentage of your account.

TradersPost.io succinctly explains this: "ATR-based position sizing maintains consistent risk levels across varying market conditions. By scaling position sizes inversely to current volatility, traders maintain steady dollar risk regardless of whether they trade quiet or volatile markets." This dynamic adjustment is what prevents the common pitfalls of fixed sizing, where "fixed sizing often results in excessive risk during volatile periods and insufficient exposure during calm markets."

The ATR Position Sizing Formula

Implementing ATR-based position sizing involves a straightforward calculation. The general formula, as outlined by multiple sources including TradingView and Capital.com, is:

Position Size = (Account Risk in Dollars) / (ATR Value × Multiplier × Point/Pip Value)Let's break down the components:

- Account Risk in Dollars: This is the absolute dollar amount you are willing to lose on a single trade. A common risk management rule is to risk no more than 1% to 2% of your total trading capital per trade. For an account with $10,000, a 1% risk would be $100.

- ATR Value: The current Average True Range for your chosen timeframe.

- Multiplier: This factor determines your stop-loss distance. Traders often use a multiplier of 1.5 to 2.0x ATR to provide a buffer against typical market noise, as Charles Schwab suggests. For swing trades, this might even be higher, such as 2.5 or 3.0x ATR, to allow for wider price fluctuations over longer holding periods.

- Point/Pip Value: The value of one point or pip for the asset you are trading (e.g., $10 per standard lot for EUR/USD).

An Illustrative Example

Consider a trader with a $20,000 account, willing to risk 1% ($200) per trade. They are looking to trade a forex pair where the current 14-period ATR is 50 pips, and they choose a 2x ATR stop-loss multiplier.

- Desired Dollar Risk: $200 (1% of $20,000)

- ATR: 50 pips

- Multiplier: 2

- Stop Distance in Pips: 50 pips * 2 = 100 pips

- Pip Value: For a standard lot of most major forex pairs, 1 pip = $10

- Position Size Calculation: $200 / (100 pips * $10/pip) = 0.20 standard lots

FXNX provides a similar example: "If the market suddenly becomes twice as volatile (ATR jumps to 80 pips), your stop becomes 160 pips, and your lot size would drop to 0.06 lots. By reducing your lot size as volatility increases, you ensure that even if you hit your (now wider) stop loss, you still only lose exactly $100." This perfectly illustrates the power of dynamic risk adjustment.

Beyond Basic Stops: Advanced ATR Applications

While position sizing is ATR's primary contribution to risk management, its utility extends to other critical aspects of trade management. Understanding how ATR behaves across different market regimes and timeframes can significantly enhance a trader's decision-making process.

Adaptive Stop-Loss Placement

One of the most immediate benefits of ATR is its use in setting intelligent stop-loss orders. Instead of arbitrary fixed distances, an ATR-based stop loss automatically adjusts to the market's current volatility, providing a "volatility buffer." If the market is volatile, the stop will be wider, giving the trade more room to breathe without being prematurely stopped out by normal price fluctuations. In calmer markets, the stop will be tighter, allowing for quicker exits if the trade moves against you.

As Oanda explains, "you can use a multiple of the ATR to judge where your stop is to be placed. Then, having determined what percentage of your account to risk, traders can work backward to determine the correct position sizing." This systematic approach aligns stop placement directly with the market's pulse, moving away from subjective or fixed-pip stops that often prove ineffective.

Informing Take-Profit Orders

ATR can also be instrumental in setting take-profit targets. In high-volatility environments, where price swings are larger, traders might set wider take-profit targets, anticipating greater potential movement. Conversely, in low-volatility conditions, tighter take-profit levels might be more realistic. Capital.com suggests, "When the volatility is high, traders may want to set the take profit order higher... and, similarly, when the volatility is low, then they may consider setting it lower." This approach ensures that profit expectations are aligned with the prevailing market environment, rather than fixed arbitrary targets.

Timeframe Sensitivity and Noise Filtering

A crucial aspect of ATR application is its timeframe dependency. As FXNX cautions, "Warning: Never use a 5-minute ATR to set a stop for a trade you plan to hold for three days. Your volatility buffer must match your intended holding period." An ATR calculated on a 4-hour chart will inherently be much larger than one calculated on a 15-minute chart. Therefore, traders must ensure that the ATR timeframe used matches their trading timeframe and holding period. For longer-term positions, considering the ATR on weekly or even monthly timeframes can provide a more appropriate measure of volatility, as Charles Schwab highlights.

This matching of timeframe allows ATR to effectively filter out "noise" that can prematurely trigger stop losses. By understanding the typical price fluctuations for a given holding period, traders can set stops that accommodate these movements, protecting their capital from minor whipsaws.

Combining ATR with Other Indicators

ATR is not designed to be a standalone trading system but rather a potent risk management tool that complements other analytical methods. Many traders combine ATR with trend-following indicators like moving averages, momentum oscillators like RSI, or classical technical analysis such as trendlines and support/resistance zones. For example, a trader might enter a position based on a moving average crossover but then size the trade and place their stop loss using ATR. This synergistic approach allows traders to harness the strengths of various tools: one for entry signals, another for dynamic risk control.

Holaprime confirms this collaborative use: "Absolutely. Many traders use ATR with moving averages, RSI, or trendlines. For example, a trader may enter based on trend direction but size the trade using ATR." This integration creates a more robust and adaptable trading strategy, capable of navigating diverse market conditions.

How Horizon Addresses This

How Horizon Addresses This

Implementing dynamic position sizing with ATR, while powerful, often requires manual calculations and diligent adherence, which can be time-consuming and prone to human error. Horizon Trade revolutionizes this process by integrating advanced risk management directly into its AI-powered platform. Traders can leverage Horizon's AI strategy generation to design custom trading strategies that inherently incorporate ATR-based position sizing rules, without needing to write a single line of code. The AI can be prompted to adjust position sizes dynamically based on real-time volatility metrics provided by the ATR, ensuring consistent dollar risk per trade.

Furthermore, Horizon's robust NautilusTrader backtesting engine allows users to rigorously test these ATR-adjusted strategies against extensive historical market data. This provides detailed performance metrics that validate the effectiveness of dynamic risk management, showcasing how consistent dollar risk can stabilize equity curves and reduce drawdowns. Once validated, these strategies can be deployed for live trading with automated execution, where Horizon's system flawlessly calculates and applies the correct position size for every trade based on the current ATR and your predefined risk parameters. This automation eliminates manual calculation errors and emotional biases, ensuring that your risk management is always executed precisely as intended, freeing traders to focus on strategy refinement rather than painstaking manual oversight.

Conclusion

The journey from an aspiring trader to a consistently profitable one is paved with a deep understanding and rigorous application of risk management principles. ATR-based position sizing stands out as a critical tool in this journey, transforming a static, often perilous, approach to capital allocation into a dynamic, adaptive system. By embracing ATR, traders move beyond merely guessing market direction and instead learn to respect and respond to what the market is actually doing in terms of volatility. This shift is, as FXNX aptly puts it, the "coming of age" moment for intermediate traders, marking a transition from reactive to proactive risk control.

By letting volatility define your risk, you protect your capital from the inherent "noise" of the markets, positioning yourself not just to survive but to thrive amidst the inevitable fluctuations. This consistent, volatility-adjusted approach is a hallmark of professional trading, offering the flexibility to manage losses effectively and capitalize on opportunities without undue exposure. To explore how dynamic risk management, fueled by AI-powered tools, can redefine your trading consistency, visit Horizon Trade and begin building strategies that adapt to the market, not just react to it. For more research-grade insights and strategies, delve into our blog.

Sources

- ATR (Average True Range) Based Position Sizing Strategies - Holaprime

- ATR Trading Strategies Guide - TradersPost.io

- What is an average true range (ATR) trading strategy? - Capital.com

- Pos Size R&ATR — Indicator by Linus_hamren - TradingView

- Tips for Using the Average True Range (ATR) Indicator in ... - Oanda

- Risk Before Returns: Position Sizing Frameworks (Fixed- ... - Medium

- ATR-based position sizing - Master Volatility in Forex Trading - FXNX

- The Average True Range Indicator and Volatility - Charles Schwab